Prediction (out of sample)¶

[1]:

%matplotlib inline

[2]:

import numpy as np

import statsmodels.api as sm

Artificial data¶

[3]:

nsample = 50

sig = 0.25

x1 = np.linspace(0, 20, nsample)

X = np.column_stack((x1, np.sin(x1), (x1-5)**2))

X = sm.add_constant(X)

beta = [5., 0.5, 0.5, -0.02]

y_true = np.dot(X, beta)

y = y_true + sig * np.random.normal(size=nsample)

Estimation¶

[4]:

olsmod = sm.OLS(y, X)

olsres = olsmod.fit()

print(olsres.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.989

Model: OLS Adj. R-squared: 0.988

Method: Least Squares F-statistic: 1326.

Date: Tue, 17 Dec 2019 Prob (F-statistic): 1.18e-44

Time: 23:39:41 Log-Likelihood: 8.4408

No. Observations: 50 AIC: -8.882

Df Residuals: 46 BIC: -1.234

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 4.8426 0.073 66.676 0.000 4.696 4.989

x1 0.5258 0.011 46.943 0.000 0.503 0.548

x2 0.5333 0.044 12.111 0.000 0.445 0.622

x3 -0.0219 0.001 -22.256 0.000 -0.024 -0.020

==============================================================================

Omnibus: 3.262 Durbin-Watson: 2.218

Prob(Omnibus): 0.196 Jarque-Bera (JB): 2.222

Skew: -0.402 Prob(JB): 0.329

Kurtosis: 3.648 Cond. No. 221.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

In-sample prediction¶

[5]:

ypred = olsres.predict(X)

print(ypred)

[ 4.29539098 4.80736761 5.27727471 5.67604936 5.98511733 6.19944471

6.32836499 6.3940456 6.42784586 6.46516473 6.53962487 6.6775485

6.8936328 7.18853511 7.54876503 7.94890079 8.35576599 8.7338804

9.05128925 9.2848133 9.42385717 9.47215005 9.44713309 9.37709381

9.29651856 9.24042651 9.23861612 9.31076928 9.46321769 9.68790257

9.96369866 10.25988507 10.54119263 10.77359851 10.92991608 10.9942616

10.96466386 10.85338805 10.68492063 10.49194626 10.30997784 10.17152178

10.10073735 10.10946733 10.19529231 10.34192817 10.52190155 10.70106359

10.84420053 10.92081924]

Create a new sample of explanatory variables Xnew, predict and plot¶

[6]:

x1n = np.linspace(20.5,25, 10)

Xnew = np.column_stack((x1n, np.sin(x1n), (x1n-5)**2))

Xnew = sm.add_constant(Xnew)

ynewpred = olsres.predict(Xnew) # predict out of sample

print(ynewpred)

[10.89466562 10.72741816 10.43998979 10.08003848 9.71029886 9.39322261

9.17568813 9.07752305 9.08664973 9.16204231]

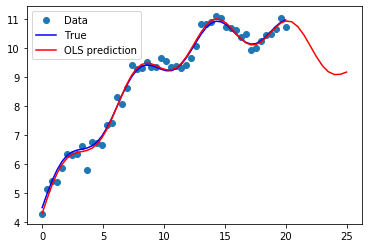

Plot comparison¶

[7]:

import matplotlib.pyplot as plt

fig, ax = plt.subplots()

ax.plot(x1, y, 'o', label="Data")

ax.plot(x1, y_true, 'b-', label="True")

ax.plot(np.hstack((x1, x1n)), np.hstack((ypred, ynewpred)), 'r', label="OLS prediction")

ax.legend(loc="best");

Predicting with Formulas¶

Using formulas can make both estimation and prediction a lot easier

[8]:

from statsmodels.formula.api import ols

data = {"x1" : x1, "y" : y}

res = ols("y ~ x1 + np.sin(x1) + I((x1-5)**2)", data=data).fit()

We use the I to indicate use of the Identity transform. Ie., we do not want any expansion magic from using **2

[9]:

res.params

[9]:

Intercept 4.842590

x1 0.525808

np.sin(x1) 0.533273

I((x1 - 5) ** 2) -0.021888

dtype: float64

Now we only have to pass the single variable and we get the transformed right-hand side variables automatically

[10]:

res.predict(exog=dict(x1=x1n))

[10]:

0 10.894666

1 10.727418

2 10.439990

3 10.080038

4 9.710299

5 9.393223

6 9.175688

7 9.077523

8 9.086650

9 9.162042

dtype: float64