Weighted Least Squares¶

[1]:

%matplotlib inline

[2]:

import numpy as np

from scipy import stats

import statsmodels.api as sm

import matplotlib.pyplot as plt

from statsmodels.sandbox.regression.predstd import wls_prediction_std

from statsmodels.iolib.table import (SimpleTable, default_txt_fmt)

np.random.seed(1024)

WLS Estimation¶

Artificial data: Heteroscedasticity 2 groups¶

Model assumptions:

Misspecification: true model is quadratic, estimate only linear

Independent noise/error term

Two groups for error variance, low and high variance groups

[3]:

nsample = 50

x = np.linspace(0, 20, nsample)

X = np.column_stack((x, (x - 5)**2))

X = sm.add_constant(X)

beta = [5., 0.5, -0.01]

sig = 0.5

w = np.ones(nsample)

w[nsample * 6//10:] = 3

y_true = np.dot(X, beta)

e = np.random.normal(size=nsample)

y = y_true + sig * w * e

X = X[:,[0,1]]

WLS knowing the true variance ratio of heteroscedasticity¶

In this example, w is the standard deviation of the error. WLS requires that the weights are proportional to the inverse of the error variance.

[4]:

mod_wls = sm.WLS(y, X, weights=1./(w ** 2))

res_wls = mod_wls.fit()

print(res_wls.summary())

WLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.927

Model: WLS Adj. R-squared: 0.926

Method: Least Squares F-statistic: 613.2

Date: Tue, 17 Dec 2019 Prob (F-statistic): 5.44e-29

Time: 23:40:04 Log-Likelihood: -51.136

No. Observations: 50 AIC: 106.3

Df Residuals: 48 BIC: 110.1

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 5.2469 0.143 36.790 0.000 4.960 5.534

x1 0.4466 0.018 24.764 0.000 0.410 0.483

==============================================================================

Omnibus: 0.407 Durbin-Watson: 2.317

Prob(Omnibus): 0.816 Jarque-Bera (JB): 0.103

Skew: -0.104 Prob(JB): 0.950

Kurtosis: 3.075 Cond. No. 14.6

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS vs. WLS¶

Estimate an OLS model for comparison:

[5]:

res_ols = sm.OLS(y, X).fit()

print(res_ols.params)

print(res_wls.params)

[5.24256099 0.43486879]

[5.24685499 0.44658241]

Compare the WLS standard errors to heteroscedasticity corrected OLS standard errors:

[6]:

se = np.vstack([[res_wls.bse], [res_ols.bse], [res_ols.HC0_se],

[res_ols.HC1_se], [res_ols.HC2_se], [res_ols.HC3_se]])

se = np.round(se,4)

colnames = ['x1', 'const']

rownames = ['WLS', 'OLS', 'OLS_HC0', 'OLS_HC1', 'OLS_HC3', 'OLS_HC3']

tabl = SimpleTable(se, colnames, rownames, txt_fmt=default_txt_fmt)

print(tabl)

=====================

x1 const

---------------------

WLS 0.1426 0.018

OLS 0.2707 0.0233

OLS_HC0 0.194 0.0281

OLS_HC1 0.198 0.0287

OLS_HC3 0.2003 0.029

OLS_HC3 0.207 0.03

---------------------

Calculate OLS prediction interval:

[7]:

covb = res_ols.cov_params()

prediction_var = res_ols.mse_resid + (X * np.dot(covb,X.T).T).sum(1)

prediction_std = np.sqrt(prediction_var)

tppf = stats.t.ppf(0.975, res_ols.df_resid)

[8]:

prstd_ols, iv_l_ols, iv_u_ols = wls_prediction_std(res_ols)

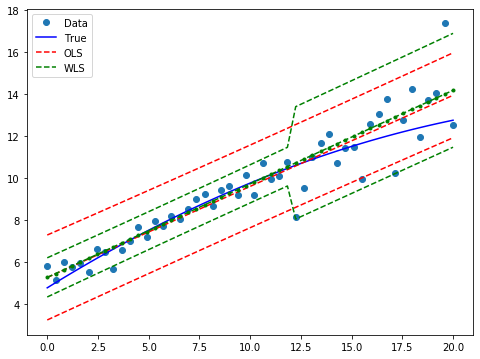

Draw a plot to compare predicted values in WLS and OLS:

[9]:

prstd, iv_l, iv_u = wls_prediction_std(res_wls)

fig, ax = plt.subplots(figsize=(8,6))

ax.plot(x, y, 'o', label="Data")

ax.plot(x, y_true, 'b-', label="True")

# OLS

ax.plot(x, res_ols.fittedvalues, 'r--')

ax.plot(x, iv_u_ols, 'r--', label="OLS")

ax.plot(x, iv_l_ols, 'r--')

# WLS

ax.plot(x, res_wls.fittedvalues, 'g--.')

ax.plot(x, iv_u, 'g--', label="WLS")

ax.plot(x, iv_l, 'g--')

ax.legend(loc="best");

Feasible Weighted Least Squares (2-stage FWLS)¶

Like w, w_est is proportional to the standard deviation, and so must be squared.

[10]:

resid1 = res_ols.resid[w==1.]

var1 = resid1.var(ddof=int(res_ols.df_model)+1)

resid2 = res_ols.resid[w!=1.]

var2 = resid2.var(ddof=int(res_ols.df_model)+1)

w_est = w.copy()

w_est[w!=1.] = np.sqrt(var2) / np.sqrt(var1)

res_fwls = sm.WLS(y, X, 1./((w_est ** 2))).fit()

print(res_fwls.summary())

WLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.931

Model: WLS Adj. R-squared: 0.929

Method: Least Squares F-statistic: 646.7

Date: Tue, 17 Dec 2019 Prob (F-statistic): 1.66e-29

Time: 23:40:04 Log-Likelihood: -50.716

No. Observations: 50 AIC: 105.4

Df Residuals: 48 BIC: 109.3

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 5.2363 0.135 38.720 0.000 4.964 5.508

x1 0.4492 0.018 25.431 0.000 0.414 0.485

==============================================================================

Omnibus: 0.247 Durbin-Watson: 2.343

Prob(Omnibus): 0.884 Jarque-Bera (JB): 0.179

Skew: -0.136 Prob(JB): 0.915

Kurtosis: 2.893 Cond. No. 14.3

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.