SARIMAX: Model selection, missing data¶

The example mirrors Durbin and Koopman (2012), Chapter 8.4 in application of Box-Jenkins methodology to fit ARMA models. The novel feature is the ability of the model to work on datasets with missing values.

[1]:

%matplotlib inline

[2]:

import numpy as np

import pandas as pd

from scipy.stats import norm

import statsmodels.api as sm

import matplotlib.pyplot as plt

[3]:

import requests

from io import BytesIO

from zipfile import ZipFile

# Download the dataset

dk = requests.get('http://www.ssfpack.com/files/DK-data.zip').content

f = BytesIO(dk)

zipped = ZipFile(f)

df = pd.read_table(

BytesIO(zipped.read('internet.dat')),

skiprows=1, header=None, sep='\s+', engine='python',

names=['internet','dinternet']

)

Model Selection¶

As in Durbin and Koopman, we force a number of the values to be missing.

[4]:

# Get the basic series

dta_full = df.dinternet[1:].values

dta_miss = dta_full.copy()

# Remove datapoints

missing = np.r_[6,16,26,36,46,56,66,72,73,74,75,76,86,96]-1

dta_miss[missing] = np.nan

Then we can consider model selection using the Akaike information criteria (AIC), but running the model for each variant and selecting the model with the lowest AIC value.

There are a couple of things to note here:

When running such a large batch of models, particularly when the autoregressive and moving average orders become large, there is the possibility of poor maximum likelihood convergence. Below we ignore the warnings since this example is illustrative.

We use the option

enforce_invertibility=False, which allows the moving average polynomial to be non-invertible, so that more of the models are estimable.Several of the models do not produce good results, and their AIC value is set to NaN. This is not surprising, as Durbin and Koopman note numerical problems with the high order models.

[5]:

import warnings

aic_full = pd.DataFrame(np.zeros((6,6), dtype=float))

aic_miss = pd.DataFrame(np.zeros((6,6), dtype=float))

warnings.simplefilter('ignore')

# Iterate over all ARMA(p,q) models with p,q in [0,6]

for p in range(6):

for q in range(6):

if p == 0 and q == 0:

continue

# Estimate the model with no missing datapoints

mod = sm.tsa.statespace.SARIMAX(dta_full, order=(p,0,q), enforce_invertibility=False)

try:

res = mod.fit(disp=False)

aic_full.iloc[p,q] = res.aic

except:

aic_full.iloc[p,q] = np.nan

# Estimate the model with missing datapoints

mod = sm.tsa.statespace.SARIMAX(dta_miss, order=(p,0,q), enforce_invertibility=False)

try:

res = mod.fit(disp=False)

aic_miss.iloc[p,q] = res.aic

except:

aic_miss.iloc[p,q] = np.nan

For the models estimated over the full (non-missing) dataset, the AIC chooses ARMA(1,1) or ARMA(3,0). Durbin and Koopman suggest the ARMA(1,1) specification is better due to parsimony.

For the models estimated over missing dataset, the AIC chooses ARMA(1,1)

Note: the AIC values are calculated differently than in Durbin and Koopman, but show overall similar trends.

Postestimation¶

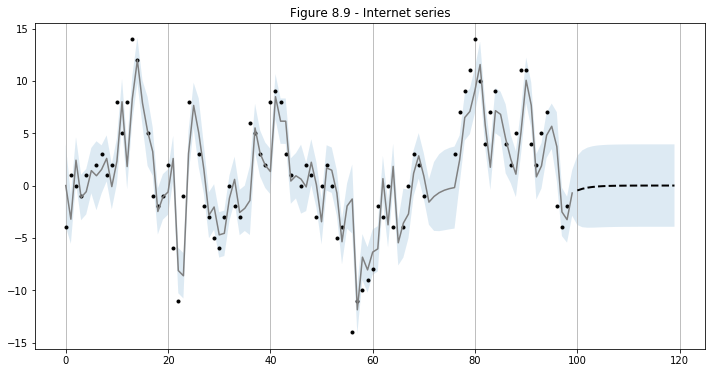

Using the ARMA(1,1) specification selected above, we perform in-sample prediction and out-of-sample forecasting.

[6]:

# Statespace

mod = sm.tsa.statespace.SARIMAX(dta_miss, order=(1,0,1))

res = mod.fit(disp=False)

print(res.summary())

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 99

Model: SARIMAX(1, 0, 1) Log Likelihood -225.770

Date: Tue, 17 Dec 2019 AIC 457.541

Time: 23:41:53 BIC 465.326

Sample: 0 HQIC 460.691

- 99

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.6562 0.092 7.125 0.000 0.476 0.837

ma.L1 0.4878 0.111 4.390 0.000 0.270 0.706

sigma2 10.3402 1.569 6.591 0.000 7.265 13.415

===================================================================================

Ljung-Box (Q): 36.52 Jarque-Bera (JB): 1.87

Prob(Q): 0.63 Prob(JB): 0.39

Heteroskedasticity (H): 0.59 Skew: -0.10

Prob(H) (two-sided): 0.13 Kurtosis: 3.64

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[7]:

# In-sample one-step-ahead predictions, and out-of-sample forecasts

nforecast = 20

predict = res.get_prediction(end=mod.nobs + nforecast)

idx = np.arange(len(predict.predicted_mean))

predict_ci = predict.conf_int(alpha=0.5)

# Graph

fig, ax = plt.subplots(figsize=(12,6))

ax.xaxis.grid()

ax.plot(dta_miss, 'k.')

# Plot

ax.plot(idx[:-nforecast], predict.predicted_mean[:-nforecast], 'gray')

ax.plot(idx[-nforecast:], predict.predicted_mean[-nforecast:], 'k--', linestyle='--', linewidth=2)

ax.fill_between(idx, predict_ci[:, 0], predict_ci[:, 1], alpha=0.15)

ax.set(title='Figure 8.9 - Internet series');