Autoregressive Moving Average (ARMA): Artificial data¶

[1]:

%matplotlib inline

[2]:

import numpy as np

import statsmodels.api as sm

import pandas as pd

from statsmodels.tsa.arima_process import arma_generate_sample

np.random.seed(12345)

Generate some data from an ARMA process:

[3]:

arparams = np.array([.75, -.25])

maparams = np.array([.65, .35])

The conventions of the arma_generate function require that we specify a 1 for the zero-lag of the AR and MA parameters and that the AR parameters be negated.

[4]:

arparams = np.r_[1, -arparams]

maparams = np.r_[1, maparams]

nobs = 250

y = arma_generate_sample(arparams, maparams, nobs)

Now, optionally, we can add some dates information. For this example, we’ll use a pandas time series.

[5]:

dates = sm.tsa.datetools.dates_from_range('1980m1', length=nobs)

y = pd.Series(y, index=dates)

arma_mod = sm.tsa.ARMA(y, order=(2,2))

arma_res = arma_mod.fit(trend='nc', disp=-1)

/home/travis/build/statsmodels/statsmodels/statsmodels/tsa/base/tsa_model.py:162: ValueWarning: No frequency information was provided, so inferred frequency M will be used.

% freq, ValueWarning)

[6]:

print(arma_res.summary())

ARMA Model Results

==============================================================================

Dep. Variable: y No. Observations: 250

Model: ARMA(2, 2) Log Likelihood -353.445

Method: css-mle S.D. of innovations 0.990

Date: Tue, 17 Dec 2019 AIC 716.891

Time: 23:40:00 BIC 734.498

Sample: 01-31-1980 HQIC 723.977

- 10-31-2000

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1.y 0.7904 0.134 5.878 0.000 0.527 1.054

ar.L2.y -0.2314 0.113 -2.044 0.041 -0.453 -0.009

ma.L1.y 0.7007 0.127 5.525 0.000 0.452 0.949

ma.L2.y 0.4061 0.095 4.291 0.000 0.221 0.592

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.7079 -1.1851j 2.0788 -0.0965

AR.2 1.7079 +1.1851j 2.0788 0.0965

MA.1 -0.8628 -1.3108j 1.5693 -0.3427

MA.2 -0.8628 +1.3108j 1.5693 0.3427

-----------------------------------------------------------------------------

[7]:

y.tail()

[7]:

2000-06-30 0.173211

2000-07-31 -0.048325

2000-08-31 -0.415804

2000-09-30 0.338725

2000-10-31 0.360838

dtype: float64

[8]:

import matplotlib.pyplot as plt

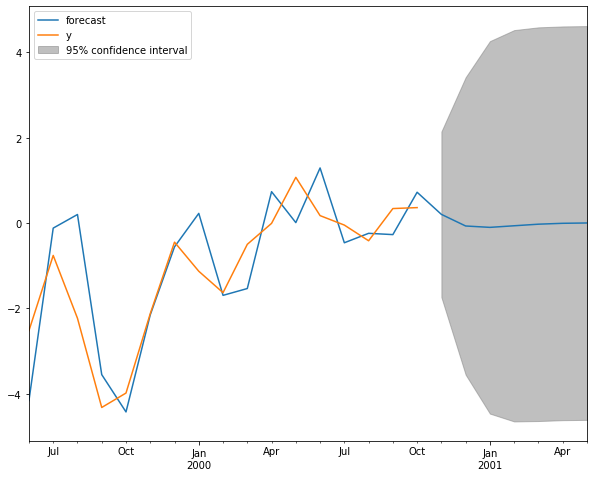

fig, ax = plt.subplots(figsize=(10,8))

fig = arma_res.plot_predict(start='1999-06-30', end='2001-05-31', ax=ax)

legend = ax.legend(loc='upper left')